A howler from the IPPR

The IPPR have a report out today calling for corporation tax to be hiked and employers’ national insurance contributions to be cut. You don’t have to read far in the report to spot an absolute howler.

From the report’s Executive Summary (emphasis my own):

“The corporation tax rate should be increased, and the proceeds used to fund a reduction in employers’ national insurance contributions (ENICs). We model a rise in corporation tax from 19 to 24 per cent, which would allow a reduction in ENICS from 13.8 to 11.8 per cent. This change will ensure that shareholders bear a greater portion of the burden of corporate taxation, allowing the proceeds to be passed on to workers through wage increases or additional employment. A higher rate of corporation tax would also raise the value of investment allowances, creating a larger incentive for investment. The changes would shift the burden of taxation away from less profitable businesses with high input costs onto more profitable ones”

Let’s put it to one side whether shifting taxation from businesses with high input costs to businesses with low input costs is a good idea. The idea that a higher rate of corporation tax increases the incentive to invest is categorically wrong.

Guys. It’s time for some optimal tax theory.

In the 1960s Dale Jorgenson and Robert Hall put together a framework for evaluating the effect taxes have on investment. It’s pretty straightforward. It sums up all the associated costs of capital such as taxes, depreciation and borrowing costs. If an investment can generate a return net of those costs then it’ll take place, if it doesn’t then it won’t be made.

The amazing thing about Hall and Jorgenson’s User Cost of Capital equation is that it lets you mathematically prove that the IPPR’s claim that higher rates of corporation tax will increase the incentive to invest is wrong.

Alan Cole (formerly of the Tax Foundation) in his paper Fixing the Corporate Income Tax, shows that raising the corporate tax rate increases the cost of capital.

“Hall and Jorgenson derive an expression for the price of capital, as follows:[10]

“where c is the cost of capital services, q is the price of capital goods, r is the discount rate, delta is the rate of physical depreciation on the asset, k is an investment tax credit, z is the present value of the depreciation deduction on one dollar’s investment, and u is the tax rate. For the purposes of this analysis, we will concern ourselves with the relationship between z and u.

“The value of z under current law is greater than zero, but less than one. A value of zero would correspond to no deductions at all, whereas a value of one would correspond to a system where deductions for capital equipment were taken immediately. (This is also often known as “expensing.”)

“Recent Tax Foundation research found z to be 0.8714 in the U.S. in 2012, meaning that the present value of the depreciation deduction schedule for the average investment made in 2012 was only about 87 percent of the value of the actual investment.

“With a value of 0.8714 for z, we find that the cost of capital increases as u increases. That is to say, a higher corporate rate (under current depreciation schedules) increases the cost of capital."

It’s true that as the net present value of capital allowances increases the effect that a higher rate has on the cost of capital falls (capital allowances also become increasingly expensive). If we allowed firms to immediately write-off capital investments (known amongst wonks as full expensing), then the corporate tax rate would have no effect whatsoever on investment, but at no point does a higher corporate tax rate increase the incentive to invest. The IPPR’s claim is simply false.

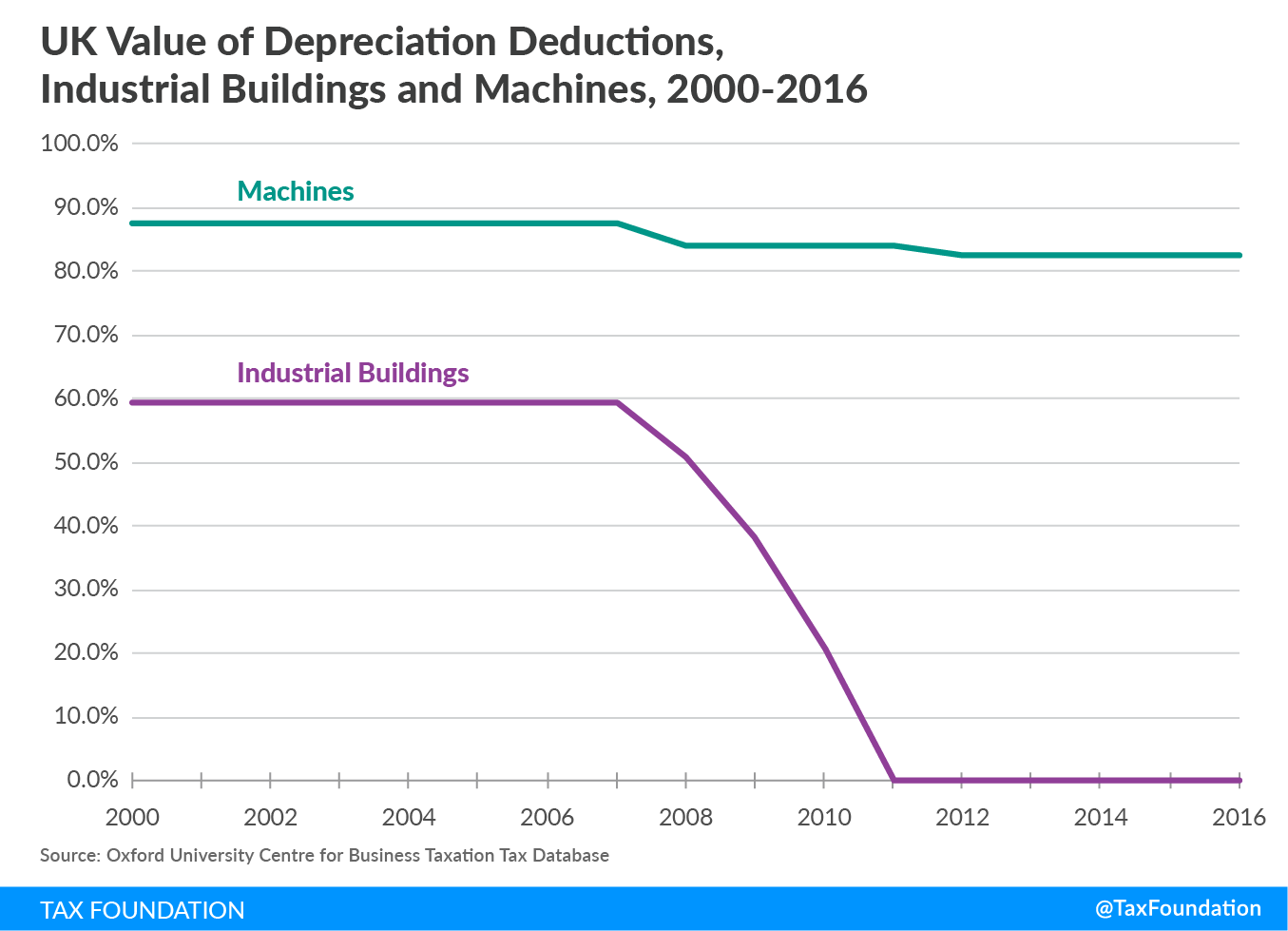

George Osborne’s 9 percentage point cut in corporation tax was funded in part by making depreciation schedules less generous (and in the case of industrial buildings scrapped them altogether).

As a result, the UK’s Effective Marginal Tax Rate in 2016 was only 3% lower than in 2007. Osborne’s rate cuts were effective at attracting international capital, but failed to move the needle on domestic investment. Hiking corporation tax without expanding capital allowances (which is what the IPPR propose) would hit investment hard.